- by New Deal democrat

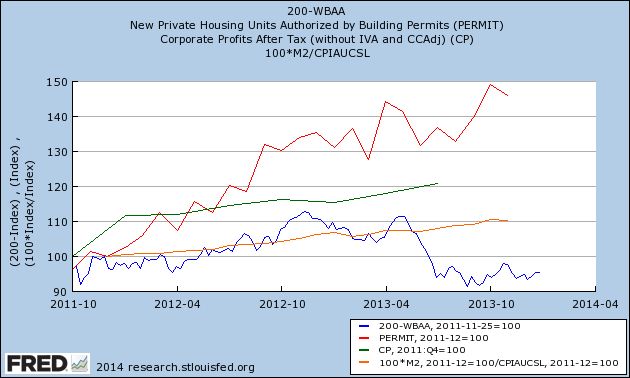

I have a new post up at XE.com, commenting on recent speculation about a stock market crash vs. a pullback due to valuations in 2014, based on YoY corporate profits in 2013.

demographics and household formation suggest starts will return to close to the 1.5 million per year average from 1959 through 2000. That means starts will come close to increasing 60% over the next few years from the 2013 level.From there he deduces his forecast of 20% this year.